Introduction to Taxation in India

Introduction to Taxation in India

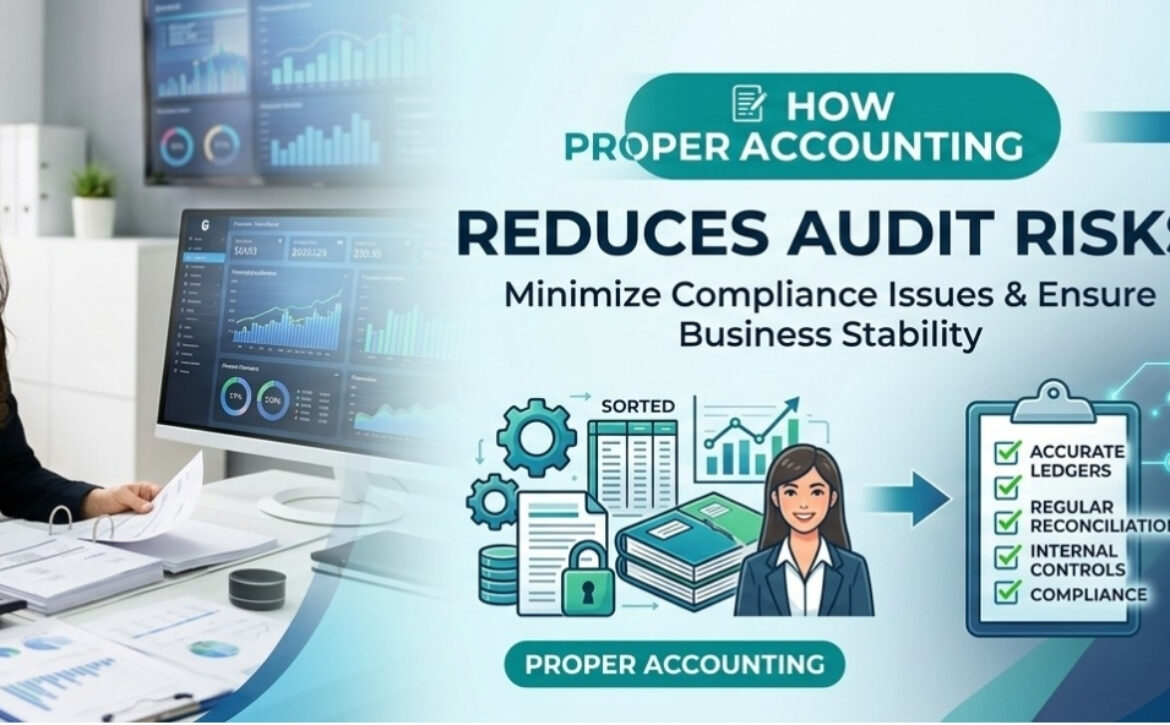

Why Accurate Accounting Reduces Audit Risk is an important concept in today’s world of business. Businesses must ensure that their financial records are accurate at all times. Therefore, in business, accurate accounting is an effective means of preventing errors and compliance problems. Additionally, a business’s ability to have good accounting practices will enable it to increase its financial controls and transparency. The regulatory environment of India has increased regulations, which create pressure on businesses to have strong accounting programs to assist in risk reduction.

How Accurate Accounting Reduces Audit Risk

The first step in How Accurate Accounting Reduces Audit Risk is to create accurate financial records. Every transaction needs to be tracked accurately by a business. Consequently, good accounting practices create organized financial records for businesses. When a business’s financial records are organized and accurate, they provide auditors with easier access to verify the accuracy of the financial statements being audited.

Lastly, the auditors will have fewer discrepancies to resolve, and any confusion regarding the accuracy of the financial records will lead to smoother and quicker audits.

Financial Accuracy and How Accurate Accounting Reduces Audit Risk

How Accurate Accounting Reduces Audit Risk provides consistent financial accuracy. Errors are made in accounting, which can cause concern for auditors regarding the accuracy of the financial statement(s). Accurate accounting will provide an audit with a business owner with accurate accounting records to prevent an audit from taking place. Additionally, good accounting practices help identify discrepancies between actual and projected revenues and expenses consistently.

Lastly, businesses significantly reduce their audit risk when they have good accounting records in place to provide accurate financial reporting.

Compliance and How Proper Accounting Reduces Audit Risks

The way in which proper accounting decreases audit risk, efficient compliance with regulations, is demonstrated through Correct tax law compliance, proper tax reporting compliance, and timely submission of accurate business records in order for a business to successfully file its taxes.

When an organization has accurate and complete records on file that can be used to verify compliance, it reduces its exposure to tax-related fines or penalties imposed by the government, which leads to continued credibility with all levels of government.

Documentation and How Proper Accounting Reduces Audit Risks

Reference to Proper Documentation. Where a business uses proper documentation, the accuracy of the accounting records is dependent on appropriate documentation, as examples of proper documentation include but are not limited to invoices, receipts, and financial statements, which help businesses maintain audit readiness by providing auditors with the required clarity of documentation during their review of business records. It also gives the auditor confidence in their review of the business records.

Internal Controls and How Proper Accounting Reduces Audit Risks

Reference Internal Controls. When a business uses strong internal controls, the effectiveness of its internal controls improves the operation of the accounts payable and receivable processes through checks and balances, which reduces the business’s exposure to errors and decreases the likelihood of fraud.

The organization reviews the effectiveness of its internal controls on a regular basis to ensure that they comply with the organization’s internal policies and procedures, which will in turn serve to enhance accountability across all departments and improve the business’s ability to effectively manage its audit risk.

Using Technology to Reduce Audit Risk

Accounting functions can greatly benefit from advancements in technology. With automated accounting systems, companies are now able to perform financial transactions without creating a significant number of errors. In addition to increasing the speed and efficiency of financial transactions, automated accounting systems provide businesses with current financial information from their cloud-based systems. By using automated systems and cloud-based technologies, businesses have the ability to produce consistent financial reports, which together enhance a company’s readiness for external audits.

Managing Risks Using Proper Accounting

The key to effective risk management is proper accounting practices. On the contrary, when a business has poor or incorrectly written accounting records, it creates uncertainty or risk associated with finances.

To manage risks effectively, businesses must conduct regular financial statement reviews. Conducting regular reviews of a business’s financial records enables businesses to find and resolve issues before they become serious problems. By resolving issues before they become serious, businesses can take proactive measures to prevent the risk of loss associated with the financial statements.

The Benefits of Proper Accounting to Reduce Audit Risk

There are many benefits associated with having proper accounting practices. By having proper accounting practices, businesses are able to organize financial records and improve the operational efficiency of the business, and therefore, businesses will become more functionally successful in the marketplace.

Additionally, businesses that utilize proper accounting practices create a higher level of trust with stakeholders and government agencies and therefore have improved confidence in their ability to make decisions that will result in sustained success.

Using an Outsourcing Service to Reduce Audit Risk

Outsourcing your accounting services to a qualified third party (CPA or accounting firm) can help your business reduce audit risk. The use of outsourced accounting services will provide businesses with professional accountants who can verify and provide accurate financial statements. In addition to improving the accuracy of the financial statements, outsourced accounting firms also allow businesses to reduce the amount of work required to prepare financial statements, significantly improving the overall audit risk associated with an entity.

Proper Accounting Reduces Audit Risk is vital to becoming a successful business. Accurate records provide the necessary basis for maintaining compliance with regulations and transparency.

Accordingly, businesses need to have robust accounting policies. By establishing proper accounting, companies can prevent issues related to audits. Ultimately, sound accounting creates a solid foundation to support their growth and success.